What are the hallmarks of a well-built investment portfolio? Low cost, broad diversification, tax-efficiency, risk compatibility with the owner, and performance that matches or beats an apples-to-apples yardstick.

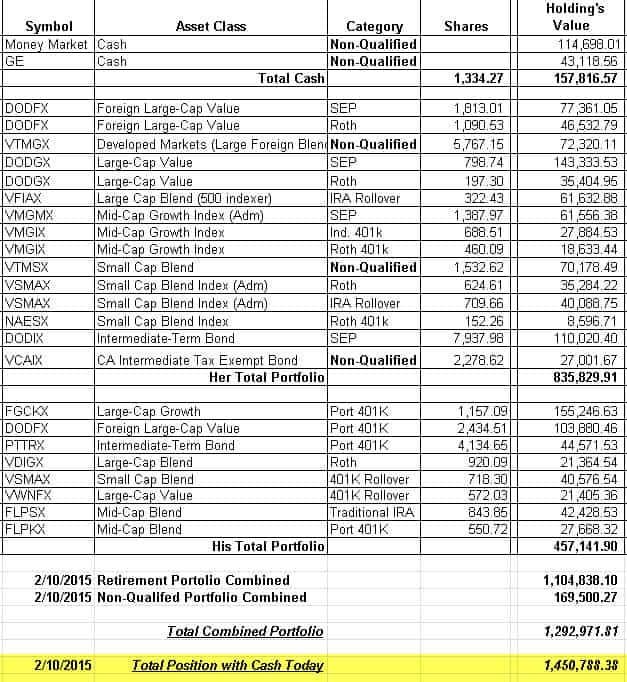

My latest Portfolio Report Card is for a married couple, C.J. in Orange County, CA. He is 57, she is 58 and they asked me to grade their combined $1.45 million investment portfolio. He works in the transportation business and she’s a fundraiser.

(Audio) Listen to Ron DeLegge @ The Index Investing Show

C.J. told me they manage their own money and consider themselves moderate risk takers with growth of money more important than current income. Altogether, C.J.’s owns 16 mutual funds and one individual stock (General Electric).

Their investment time horizon before retiring is 9 years.

C.J.’s combined $1.45 portfolio are scattered across different IRAs, 401(k) plans, rollovers from a previous job and a taxable account. Do they have a healthy or unhealthy investment plan?

Let’s do a Portfolio Report Card for C.J. and find out.

Cost

The combined fund expenses range from 0.09% (low end) to 0.82% (high end) and are controlled. C.J. has accomplished this cost-cutting mission by using low cost index funds covering large stocks (Nasdaq:VFIAX), midcaps (Nasdaq:VMGMX), and developed markets (Nasdaq:VTMGX).

Diversification

C.J.’s portfolio has exposure to foreign and US stocks, bonds (Nasdaq:PTTRX) and cash. Well done!

Still, it misses exposure to major areas or asset classes like emerging market stocks, commodities, and real estate. Remember: Broad diversification should always happen before investing in any individual securities like General Electric (NYSE:GE) and others.

Risk

The overall asset mix of this total combined portfolio is the following: 79.5% stocks, 12.5% bonds, and 8% cash. This is a high risk asset mix – even for late 50s “aggressive” investors. A 20% to 40% decline would subject this portfolio to potential losses from $230,000 to $460,000. C.J. privately acknowledged they need to dial down risk.

Snapshot of C.J.’s Combined Portfolios

Tax Efficiency

All investment portfolios, whether taxable or tax-deferred accounts, should be built to minimize the negative impact of taxes to the greatest degree possible. The overall tax-efficiency is excellent. C.J. has executed 401(k) rollovers and hasn’t made any pre-mature retirement distributions or other activity that could subject them to unwanted taxes and penalties. Outstanding work!

Performance

This portfolio grew 9.9% from Feb. 2014 to Feb. 2015 versus a +10.95% gain for our blended index benchmark matching this same asset mix. Performance came close to matching our index benchmark and is satisfactory.

The Final Grade

C.J.’s final Portfolio Report Card is “B.” While not a perfect grade, it means this portfolio scored well in most grading categories.

C.J. scored best on cost, tax-efficiency and performance. However, diversification is sloppy and misses major asset classes like emerging market stocks (NYSEARCA:VWO), commodities (NYSEARCA:DBC), and real estate (NYSEARCA:VNQI).

The risk profile of this portfolio is hyper-aggressive and doesn’t match “aggressive” investors in their late 50s. I estimate a 20%-40% market decline would subject this portfolio to significant volatility and potential losses.

The good news is that C.J. are outstanding savers. And if they can tweak their investment plan, they’ll have a more robust portfolio with better balance and stability.

Ron DeLegge is the Founder and Chief Portfolio Strategist at ETFguide. He’s inventor of the Portfolio Report Card which helps people to identify the strengths and weaknesses of their investment account, IRA, and 401(k) plan.

Follow Ron’s new podcast Portfolio Talk on Twitter @PTalkRadio